Global Finance Market

The US economy is going through a doom, and it goes without saying that it has impacted the entire world’s financial market. The month of September 2008 has witnessed colossal plunge in the finance market. Top investment giants have been nailed down; the fourth largest investment bank of the world: Lehman Bros. filed for bankruptcy, sale of Merill Lynch to Bank of America; and AIG Inc raising money to survive. The market sentiments have become vulnerable; everybody is left guessing what next?? Though regulators are now making efforts to stabilize the market; but it is highly unpredictable and disruptive atmosphere.

The Asset backed securities (ABS) which had once witnessed a leap and bound rise, is set on a decline now. Until year 2007, a ‘Triple A’ rated bond was as good as a covered bond, but it is not the same anymore. The troubles of ABS market have made the investors more cautious and choosy. Now use of covered bonds as means of raising cheap finance is rising fast.

Covered Bonds call of the day: “Closer to the age-old concept of secured lending; and running parallel to securitisation”

As the financial market is facing a decline, a not so new mode of raising finance is on a rise. It can be said that Covered bond is only a new anatomy for the generic concept of secured lending. It owes all its basic attributes to secured lending however also reap some benefits from the concept of asset backed funding. The idea is to get the best features of the two modes of funding and develop a new means to raise finance that suits the investor’s appetite.

Investor’s choice changes with time, and so has to be with the nature of securities offered to them. Quite sometime back, it was plain simple secured lending; then there was a gush for sophisticated structured products of asset backed funding; now the buzzword for the day is Covered Bonds! Though Asset based funding is nonetheless relevant, however with the downturns of the risk appetite of investors- Covered Bonds will find a more favorable market.

Europe has been the first one to introduce covered bonds in the market in the form of mortgage bonds or pfandbriefs. Certain US issuers also have used covered bonds, the first one being issued by Washington Mutual in September 2006. However, developing countries are yet to come in terms with this change.

Unique features of Covered Bonds

Certain features of covered bonds are as follows:

No off balance sheet funding: The underlying assets continue to remain on the balance sheet of the originator¹. There is no transfer of assets to a bankruptcy remote entity as in the case of asset backed funding. The issuer of bonds continues to hold the portfolio of assets, and carries the risk of default.

Dual Recourse: A very significant and distinct feature of Covered Bonds is that in the event of default of the loans, the bondholders have recourse against the pool of loans over which security has been created and also against the issuer.

Desired Rating: Inspite of the fact that the rating of covered bonds can be highly influenced by the rating of the issuer, the rating of the Covered Bonds is usually higher than that of the issuer. Issuing covered bonds can also fetch the desired rating for the securities since dual recourse against the pool of assets and highly regulated financial institution enhances the credit rating of the bonds. Further overcollateralisation, third party guarantee can be some of the other forms of credit enhancements in case of Covered Bonds.

Dynamic Pool: The cover pool of assets is mostly dynamic, i.e. the issuer can change the make-up of the loan pool to maintain its credit quality, which can benefit investors. The issuer can also change the terms of the loans thus continuing to control the underlying assets. The pool of assets is separable in case of insolvency of issuer for the benefit of the bondholders, such that the bondholders have first and foremost recourse to the pool of assets.

Multiple Issues: A very unique feature of covered bonds is that from a common pool of cover assets, more than one issue can be made. The issues may or may not rank pari passu in respect of the charge on the underlying assets, and hence may seek rating according to the pool cover.

Market of Covered Bonds

Europe being the senior most in the run has been leading with the maximum issues of covered bonds. Undoubtedly US have also geared up to experiment covered bonds with the changing investor’s behavior. The idea is yet to sink in with issuers in several countries, and there is a likelihood that the market for covered bonds in other parts of world will catch up soon. The financial regulators are also doing their bit in promoting covered bonds and reviving investor’s faith.

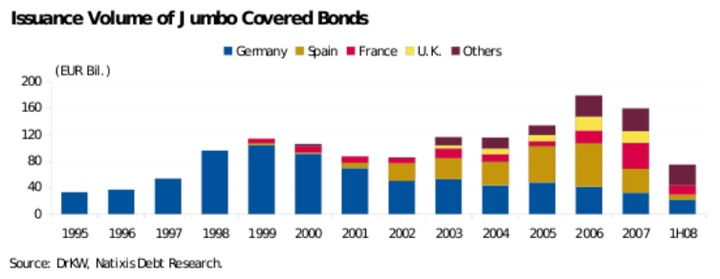

Germany has been the topnotch in issue of covered bonds with the maximum amount of outstanding covered bonds over more than 10 years. Spain and France are also inclined towards use of covered bonds. The market of covered bonds is illustrated through the below pictures² :

{kind=link}

Legal Regime

Most of the European countries have their own separate set of law governing issue of covered bonds, stating the eligible underlying assets, priority right of bondholders etc. US Treasury came up with Best Practices guidelines on covered bonds referring to two options for their issue: the direct issue of covered bonds by the issuer holding the cover pool assets on its balance sheet and an indirect issue through the creation of a special purpose vehicle.

However no specific legislation exists in most of the non-European countries that have ventured into covered bonds, such countries operate mostly under a contractual framework. Uniform Commercial Code (UCC) provides the legal background for creating a first-priority security interest over pledged assets, thus providing the broad legal background for issue of Covered bonds in countries which have no specific legislation for the same.

Is India ready for Covered Bonds?

Witnessing the low in the markets, it’s quite likely that issuers will resort to alternate and more attractive means of raising finance. However lack of understanding may pose a hindrance in the growth of the covered bonds. Further covered bonds also lack some of the attractive features of asset backed funding, such as: capital relief, off balance sheet treatment for accounting purposes, isolation of pool of assets from issuer, limiting the risk of the issuer etc. It might be less attractive to issuers however it is undoubtedly more appealing to investors especially when the sentiments of the market are significantly low.

¹Originator here refers to the entity holding the portfolio of assets securing the covered bonds

²Extracted from Fitch report “ABCs US Covered Bonds” dated September 3, 2008

2 replies on “Covered Bonds: A Primer”

Well said

How soon will you update your blog? I’m interested in reading some more information on this issue.